The 15-Year Journey of Corporate Social Responsibility (CSR) in India

-

0 Comments

Evolution of CSR in India

In pursuit of inclusive growth, India has prioritized Corporate Social Responsibility (CSR) as a vital component of its development strategy. This initiative aims to integrate social, environmental, and human development considerations across corporate value chains. The Ministry of Corporate Affairs (MCA) took the initial step by issuing the ‘Voluntary Guidelines on Corporate Social Responsibility, 2009,’ marking the beginning of mainstreaming business responsibilities.

Subsequently, these guidelines evolved into the ‘National Voluntary Guidelines on Social, Environmental, and Economic Responsibilities of Business, 2011’ (NVG Guidelines). This framework comprised nine principles designed to guide Indian businesses in adopting responsible conduct. However, recognizing the evolving landscape of sustainable business practices nationally and globally, the NVG Guidelines were revised and released as the ‘National Guidelines on Responsible Business Conduct’ (NGRBC) in March 2019.

The NGRBC aligns with international standards such as the United Nations Guiding Principles on Business & Human Rights (UNGPs), UN Sustainable Development Goals (SDGs), and the Paris Agreement on Climate Change. It provides a comprehensive framework for companies to pursue inclusive and sustainable growth while addressing stakeholder concerns effectively.

Is CSR a Successful Endeavour?

In the fiscal year 2021-22, Maharashtra emerged as the leading spender in Corporate Social Responsibility (CSR), accounting for approximately 20% of the total CSR expenditure amounting to INR 26,279 crore. Following Maharashtra, Karnataka ranked second, with Gujarat in third place, Tamil Nadu in fourth, Uttar Pradesh in fifth, and Delhi in sixth place in terms of CSR spending. Notably, the private sector contributed more than 83% of the total CSR expenditure for the year.

The data also highlights the significant allocation of CSR funds towards the health sector, which accounted for approximately 29% of the total expenditure, making it the top-spending sector. The education sector followed closely, securing the second position with a 25% share of the CSR expenditure.

These figures underscore the effectiveness of CSR initiatives as a nationwide effort, reflecting a substantial investment in social development across various sectors.

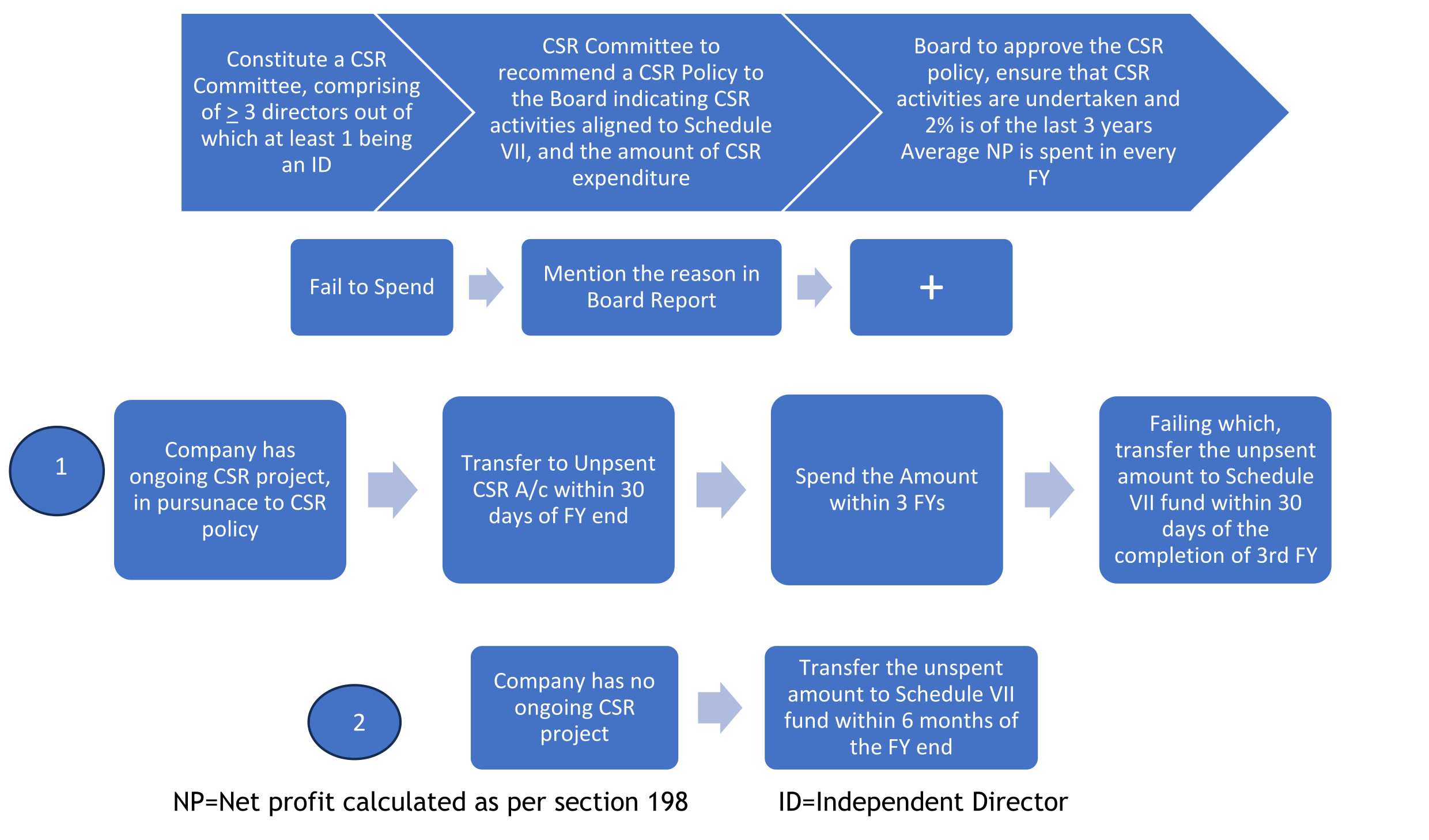

Quantum and Mode of CSR Spending

In cases where a company is not mandated to appoint an independent director under section 149(4), its CSR committee must consist of two or more directors. If a company’s CSR expenditure does not exceed fifty lakh rupees, it is not obligated to form a CSR committee. Instead, the Board assumes the responsibilities outlined for such a committee.

The activities outlined in Schedule VII encompass a wide range of items and should be interpreted liberally to capture their essence. An illustrative list of these activities was provided in MCA circular no. 21/2014 dated 18.06.20214. However, CSR activities should be undertaken in a project/programme format as per Rule 4(1) of the Companies CSR Rules, 2014. One-time events like marathons, awards, charitable contributions, advertisements, or sponsorships of TV programmes do not qualify as CSR expenditure.

Consequences of Violation

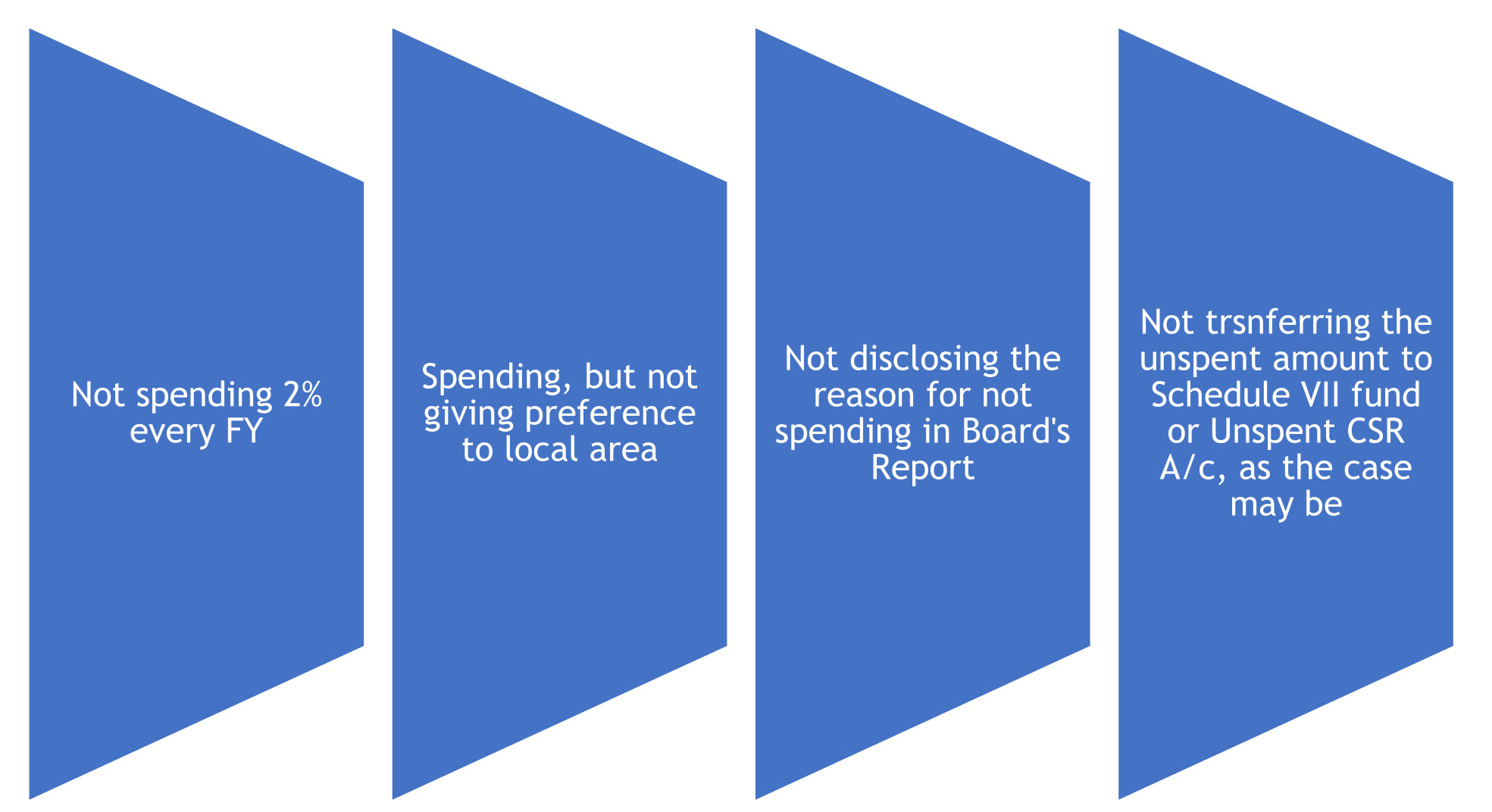

There are nine (9) sub-sections in section 135, but not adhering to all of them does not result in penalties. Sub-sections (8) and (9) are informative and do not impose any directives. Sub-section (7) specifies that non-compliance with only sub-sections (5) and (6) is punishable. It prescribes a penalty of twice the amount required for transfer to the Schedule VII Fund or Unspent CSR Account, or Rs. 1.00 Cr, whichever is less, for the company. For officers in default, the penalty is 1/10th of the required transfer amount or Rs. 2.00 Lakhs, whichever is less.

The question then arises: what scenarios could lead to non-compliance as outlined in sub-sections (5) and (6)? Let’s explore some possibilities.

Does this imply that there can be no penalty or punishment for non-compliance with sub-sections (1) to (4)? The answer is no because, in such cases, the penalty specified under section 450 would apply, which deals with punishment in the absence of specific penalties. The company, every defaulting officer, or any other person would be subject to a penalty of ten thousand rupees, with an additional penalty of one thousand rupees per day for continuing contraventions, up to a maximum of two lakh rupees for a company and fifty thousand rupees for an officer or any other person.

It’s important to note that not spending 2% of the CSR amount is not inherently punishable. If the company explains the reason for non-spending in its Board’s Report and transfers the unspent amount as required by the law, there is no immediate penalty.

Before January 22, 2021, non-compliance with CSR provisions was a criminal offense. However, to avoid discouraging companies and risking the failure of national efforts, this section was decriminalized through the Companies (Amendment) Act, 2020.

Companies Mandated to make CSR spend

Every company having any of the following three

During the immediately preceding financial year.

Every company falls under the purview of section 135, without any exemptions for Section 8 companies or foreign companies. However, specified IFSC private companies are granted a five-year exemption from the date of commencing business.

Before the Companies (Amendment) Act, 2017, companies meeting the mentioned criteria in any of the preceding three financial years were obligated to spend on CSR. However, this approach had drawbacks, as a company might have made a profit in the third preceding year but incurred losses in the previous year. This situation could discourage companies from participating in the national endeavour of inclusive growth by burdening them with CSR spending in the current financial year. Therefore, the criteria were revised to the immediately preceding financial year, effective from September 19, 2018.